[ad_1]

Main conclusions:

- If you have the funds, now may be a good time to buy a home.

- Mortgage rates are holding near 14-month lows, offering homebuyers an extended period of affordability.

- It’s a buyer’s market– there are 530,000 more home sellers than buyers – which gives home buyers an advantage.

- However, most consumers cautiously due to record high home prices, a sluggish labor market and economic uncertainty leading to a gloomy housing market.

The years may have changed, but the housing market has not. After a very slowly 2025, same thing sluggish tendencies few home sales, limited listings and record high prices persist into the new year. Economic uncertainty adds to the tension.

But there is a silver lining. Mortgage rates have continued to rise for months and are forecast to remain lower in 2026, helping homebuyers afford thousands more than they could last year.

A lot is changing, so it’s no wonder buyers are wondering if now is the time to make the leap.

In short, the right time to buy a home depends on how convenient the time is for you buy a house. Let’s delve into today’s market trends to help you answer the question: Should you buy a home now or wait?

From Redfin’s Chief Economist

“Now is a good time to buy a home if you can afford it. Prices continue to rise, pushing people out of the market and giving buyers a bargaining chip. However, a tough economy has everyone on guard, and local housing markets vary widely. Buyers serious about making an offer should check with a local agent and be sure of their finances and future returns.” – Daryl Fairweather, Chief Economist, Redfin.

What buyers need to know about the housing market

Here are some key market trends to keep an eye on to help you make an informed choice when buying a home.

Housing prices are high and may continue to rise

The US median sales price is $429,000, up 0.6% from a year ago. House prices have been rising year-over-year for more than two years and are 30% higher than five years ago.

Since availability was very tight, so were many potential buyers holding on for better deals, causing inventory to build up. Recently, sellers began to notice, p more are pulling their homes off the market in response. This two-stroke dynamic keeps prices higher and reduces demand.

Red-cockaded predicts that prices will rise more slowly this year, which should help improve affordability as wages rise.

>> Read: Redfin Weekly Economic Report

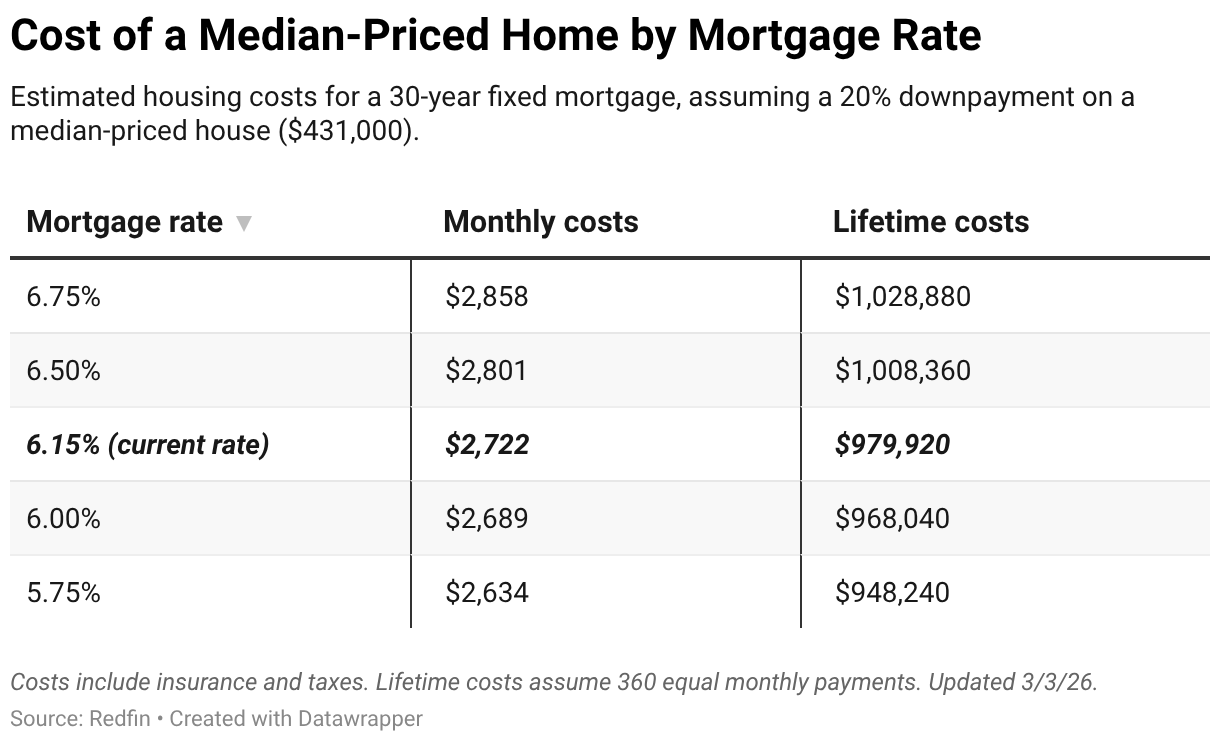

Mortgage rates continue to fall steadily

As of January 6, the fixed 30-year weekly average value mortgage rate sitting at 6.20% – lower than last week and in line with long-term declines.

“Mortgage rates have been hovering between 6.1%-6.3% for several months and we expect this to continue into 2026.” said Chen Zhao, head of economic research at Redfin. “A weak labor market will prompt the Fed to cut interest rates this year, but lingering inflation and the risk of a recession will prevent significant economic improvement. On the positive side, homebuyers are enjoying much lower interest rates than this time last year — when they topped 7% — which should continue into the spring.”

Redfin predicts that mortgage rates will be around 6.3% in 2026.

>> Read: Mortgage rates are falling. Here’s what home buyers and sellers should do about it

How mortgage rates affect home values

Mortgage rates are important to buyers because they translate directly into monthly housing costs. The higher the rate, the more you pay each month. When rates fall, you can save tens of thousands throughout the life of your mortgage.

Let’s see how your monthly payments change with different rates using our data Mortgage calculator.

Buyers have an advantage

This is the strongest buyer’s market in years: housing inventory got up from post-pandemic lows, especially in the South, giving buyers more bargaining power. However, supplies are still limited in parts of the Midwest and East Coast, putting the onus on retailers. pushing up prices.

Overall, however, high costs are keeping buyers away and freezing home sales. Some households are forced to do great sacrifices such as giving up a pet or delaying a divorce to afford housing. Younger generations suffered particularly hard and often addressing the family for help.

Let’s dig into the data and look at two key market indicators.

Inventory is high but falling

About 1.7 million homes are listed for sale today— historically low, but one of the highest December levels since the pandemic. This is the main driver of today’s buyer’s market. Florida and Texas have the most homes on the market today.

Housing inventory is high because a greater share of sellers are listing their homes than buyers are buying them, with the largest imbalance in disaster-prone areas. in Florida. This gives today’s buyers more options for concessions.

But many sellers are now starting to back out after realizing they can’t get top dollar, which is starting to thin the housing stock. Home building too dived in 2025.

Demand is near an all-time low

Even with lower rates and more homes on the market, buyer demand remains weak due to high home prices and economic uncertainty. yearbook of the National People’s Congress Profile of buyers and sellers of housing confirms this: first-time buyers are older, more cost-conscious, fewer and farther apart.

For buyers on a budget, this can be a good time to enter the market as sellers may be more open to negotiations.

Still there are exceptions. The cities of New York like it Rochester and Buffalogreat demand for available houses pushes up prices and puts responsibility on sellers. Bay Area sees a surge in popularity as well, along with parts of the Midwest.

>> Read: How to Sell Your Home in 2025: The Complete Guide

Inflation may rise

The housing market is critical, economists concerned that inflation may rise due to changes in economic and immigration policy data, which will affect mortgage rates and affordability.

Although inflation has not increased, it is there creeping up and remains above the Fed’s target; experts say it will continue to rise unless policy changes. In fact, a the report found that inflation could have fallen by about one-third if not for tariffs.

Inflation has serious consequences for buyers. The most important thing is this can lead to higher housing prices and mortgage rates, as well as further stretching of budgets. If inflation does pick up, loans could become more expensive, making this a smart move fix the rate before that happens.

>> Read: The housing market under Donald Trump: What it could mean for buyers, sellers and renters

How to buy in an uncertain economy

With tariffs, the economic shock and volatile mortgage rates, many buyers are wary of entering the market. Here are some tips from our economists on how to navigate this changing landscape.

- Stick to your budget: Now is not the time to stretch yourself financially. The chances of a recession are lower than before, but the economy is still unstable. Make sure you have enough savings to cover your mortgage payments if your income changes.

- Negotiate, negotiate: The market favors buyers, so use your leverage. The range has become larger, and more and more offers are coming from below.

- Be smart about bidding: Mortgage rates are falling, but still relatively high. Shop around, compare lenders and ask about “float down” options if the rates drop significantly after you lock in.

- Sell before you buy: If you own a home, consider selling it first. This will give you a clearer budget and help you avoid the risk of taking out two mortgages.

>> Read: How to buy, sell, or rent a home amid economic uncertainty

Are you ready to buy a home and own it?

When making a home buying decision in today’s climate, you’ll want to think beyond market conditions and focus on your personal circumstances. Here are some personal considerations to keep in mind.

Financial health

Take stock of your current savings, credit scoreand debt levels. You can afford a house? Or makes rent make more sense?

Housing is a long-term commitment, so you’ll need a solid emergency fund – ideally to cover 3 to 6 months’ worth of expenses – for maintenance and contingencies.

Monthly budget

Find out how a mortgage payment at today’s rates can affect your lifestyle. Make sure you are comfortable driving monthly payments, property taxes, insuranceand others home ownership expenses.

Stability of work and location

Buying a home makes sense if you plan to stay put for several years. A stable job or reliable income is crucial to avoid financial stress, especially if house prices or interest rates rise further.

The choice of location is also important. Is your potential home prone to floods, wildfires, or otherwise climate risks? This is especially important today, as insurers continue the fall of homeownership at an alarming rate.

Personal goals and deadlines

Think about life events like starting a family, retiring or moving. These factors can make home ownership either more attractive or potentially more risky if you need to move quickly.

Lifestyle benefits

Home ownership involves ongoing responsibilities, e.g maintenance, repairand property taxes. Ask yourself if you have the time, resources and desire to handle them.

>> Read: Am I ready to buy a house? 8 questions to help you decide

So, is now a good time to buy a home?

If you have the funds and are ready to own a home, now is a good time to do so buy a house. Rates are coming down, but with today’s high prices and volatile economy, it’s hard to predict what affordability will look like down the road. Waiting for rates to fall creates the risk of competition among buyers and subsequent price increases by sellers.

In such an unpredictable market, it’s best to be prepared. Know your budget contact your local agent, get pre-approvedand move quickly when the right home comes up. The longer you wait, the more competition you may see.

[ad_2]

Source link